U.S. government-backed mortgage bonds are heading toward their longest monthly slump since 1999 as concern mounts that the Federal Reserve will begin paring its debt purchases even as the steepest rise in home-loan rates in at least 40 years slows the

housing rebound.

Enlarge image

Pimco Sees Taper in Worst MBS Slump Since 1999: Credit Markets

Ariana Lindquist/Bloomberg

An attendee views a 1,700 square foot "empty nester" one bedroom called the Idea Home at the Minneapolis Home & Garden Show in Minnesota on March 1, 2013.

An attendee views a 1,700 square foot "empty nester" one bedroom called the Idea Home at the Minneapolis Home & Garden Show in Minnesota on March 1, 2013. Photographer: Ariana Lindquist/Bloomberg

Securities guaranteed by Fannie Mae, Freddie Mac or Ginnie Mae lost 0.33 percent through yesterday, heading for their fourth month of declines and bringing losses since April to 2.78 percent, according to Bank of America Merrill Lynch index data. For almost a year, the Fed has been adding $40 billion of

bonds to its balance sheet each month from the more than $5 trillion market. It expanded the purchases in January to include $45 billion of Treasuries.

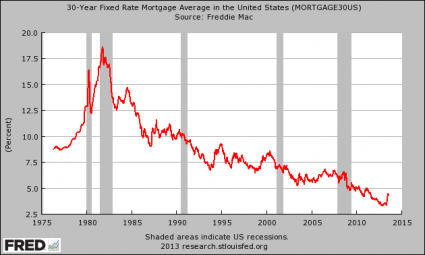

Investors led by Pacific Investment Management Co., manager of the world’s biggest bond fund, are bracing for the Fed to scale back its stimulus when policy makers meet next month, even after data the past week showed falling home sales and a slowdown in property appreciation. Average rates for 30-year mortgages reached a two-year high of 4.58 percent last week.

“We still believe that tapering is going to happen,” said Michael Cudzil, an executive vice president who specializes in mortgages at Newport Beach, California-based Pimco. “The Fed is looking at the progress seen in the data over a long-term period of time, rather than any one given month.”

Stimulus Doubts

Bolstering speculation the Fed will taper are doubts among some policy makers about how effective their balance-sheet expansion has been in boosting the economy and their concern that it may spur excessive risk-taking, he said in a telephone interview. Regional Fed presidents Esther George of Kansas City, Jeffrey Lacker of Richmond, Richard Fisher of

Dallas and Charles Plosser of Philadelphia have all spoken out against the program.

“They’ve done the work preparing markets, and they’ll probably take this as an opportunity to make the move and see how the markets react,” Cudzil said.

The slump in mortgage bonds pushed the average rate offered on new 30-year fixed home loans to 4.51 percent this week from an almost-record low 3.35 percent in early May, according to Freddie Mac surveys. The 35 percent increase over 17 weeks is the fastest in a comparable period since at least 1972.

‘Coin Toss’

In what Cudzil said may be a sign investors are anticipating a greater reduction in Treasury purchases than bonds backed by home loans, agency mortgage securities are losing less than similar-duration government debt for the second month with excess returns of 0.1 percent in August, Bank of America Merrill Lynch index data show.

“I’m definitely thinking these rising rates will impact” the housing recovery and Fed officials “must be as well,” said Joseph Galligan, a money manager at Los Angeles-based DoubleLine Capital LP, which oversees about $55 billion. While he said the central bank probably won’t act next month, “it’s a coin toss” and “if it’s skewed toward anything, I would think a reduction that’s more on the Treasury side than the mortgage side.”

Elsewhere in credit markets, the cost to protect against losses on corporate bonds in the U.S. headed for the third weekly increase this month. BC Partners Ltd., Cinven Ltd. and other private-equity companies raised 3.1 billion euros ($4.1 billion) of loans this month in Europe, the busiest August since 2007, amid signs the area’s economy has bottomed.

Apache Bonds

Bonds of Houston-based Apache Corp. are the most actively traded dollar-denominated corporate securities by dealers today, accounting for 3.5 percent of the volume of dealer trades of $1 million or more, according to Trace, the bond-price reporting system of the Financial Industry Regulatory Authority.

China Petrochemical Corp., Asia’s largest refiner, agreed to pay $3.1 billion for a 33 percent stake Apache’s Egyptian oil and gas business. Apache’s $1.5 billion of 4.75 percent bonds due in 2043 climbed 2.4 cents to 95.4 cents on the dollar as of 10 a.m. in New York, with the yield falling to 5.05 percent from 5.22, Trace data show.

The Markit CDX North American Investment Grade Index, a credit-default swaps benchmark that investors use to hedge against losses or to speculate on creditworthiness, rose 1.2 basis points to a mid-price of 83.7 basis points as of 11:46 a.m., according to prices compiled by Bloomberg. The measure has climbed 4.9 basis points this week and 9.1 in August, on pace for the biggest monthly increase since May 2012.

European Benchmark

In

London, the

Markit iTraxx Europe Index, tied to 125 companies with investment-grade ratings, rose 2.4 to 107.2, extending August’s increase to 7.3 basis points.

The indexes typically rise as investor confidence deteriorates and fall as it improves. Credit swaps pay the buyer face value if a borrower fails to meet its obligations, less the value of the defaulted debt. A basis point equals $1,000 annually on a contract protecting $10 million of debt.

Investor demand for corporate high-yield debt allowed borrowers in Europe to raise more than double the amount recorded in August 2012 and came after 7.2 billion euros of loans were signed last month, Bloomberg data show.

BC Partners got $2.6 billion of mostly covenant-light loans for its buyout of German academic publisher Springer Science & Business Media GmbH, while Cinven’s buyout of Internet domain and hosting company Host Europe Group Ltd. was backed by 255 million pounds ($394.5 million) of senior loans, according to data compiled by Bloomberg.

Taper Forecasts

Fed policy makers last month were “broadly comfortable” with Chairman Ben S. Bernanke’s plan to start reducing this year its third round of bond buying known as quantitative easing if the economy improves, with a few saying tapering might be needed soon, according to the meetings of the Federal Open Market Committee’s July 30-31 gathering released Aug. 21.

Reductions will be announced at the next FOMC meeting Sept. 17-18, according to 65 percent of economists in a Bloomberg survey conducted Aug. 9-13. That remains likely after some economic data released this month, such as jobless claims data on Aug. 15, was

better-than-expected, Barclays Plc analysts led by Nicholas Strand wrote in an Aug 23 report.

For agency mortgage bonds, the Fed’s lower buying will be especially important because there’s “no obvious source” of extra demand, they said. Banks are facing new regulations, real-estate investment trusts are unlikely to raise new capital after stock slumps and bond mutual funds are facing redemptions, the analysts said.

Home Sales

The Fed may slow its home-loan debt buying less than its Treasury acquisitions because of the signs of housing weakening and because some academic papers presented at an annual meeting in Jackson Hole,

Wyoming this month argued the Treasury buying is less impactful, according to Cudzil of Pimco, which manages $262 billion in its Total Return Fund.

Pending existing home sales dropped 1.3 percent in July, the most this year, after a 0.4 percent decrease in June, figures from the National Association of Realtors released Aug. 28 showed. Economists forecast no change in the gauge, according to a median estimate in a Bloomberg survey.

Purchases of new U.S. homes plunged 13.4 percent in July, the most in more than three years, to a 394,000 annualized pace, according to Commerce Department data released on Aug. 23. That was the weakest since October and lower than any of the forecasts by 74 economists Bloomberg surveyed.

The S&P/Case-Shiller index of property values in 20 cities released Aug. 27 showed prices rising 12.1 percent in June from the same month in 2012 after climbing 12.2 percent in the year ended in May, the biggest gain since 2006.

Refinancing Slows

Like DoubleLine’s Galligan, Pimco’s Cudzil said the Fed is most likely to equally reduce mortgages and Treasuries purchases.

Some Fed policy makers prefer owning only Treasuries, he said. Falling mortgage issuance may make it harder for the central bank to find enough bonds to buy at the current pace, and slowing debt repayments mean the asset may remain outstanding for longer on its balance sheets than officials want, he said.

With higher rates decreasing

refinancing applications in 15 of the past 16 weeks to a two-year low, paring expectations for mortgage-bond issuance, Amherst Securities Group LP analysts led by Laurie Goodman said that, without any stimulus pullback, the Fed’s buying will account for 75 percent of the type of new bonds it’s targeting by the fourth quarter.

‘Simple Math’

That “simple math” means it must “taper dramatically,” with it needing to cut purchases by 40 percent in order to maintain the 56 percent share of issuance that they accounted for in the first half, they wrote in an Aug. 21 report.

Investors shouldn’t jump to the conclusion that the Fed will need to reduce its buying to avoid disrupting the market’s liquidity, according an Aug. 23 report by Citigroup Inc. analysts led by Ankur Mehta.

Originators typically use forward contracts to sell future issuance a month or two before completing loans, meaning its growing share of buying is already occurring. At the same time, data show fewer failed trades and other measures aren’t signaling bonds are hard to find, they wrote.

“We think the Fed could modestly bias their tapering towards Treasuries in the September meeting, but the preference is unlikely to be very decisive,” they said.

Mortgage-bond prices gained this week, narrowing August losses, amid the weaker housing data and growing prospects of a military strike on

Syria by the U.S. and its allies. Ten-year Treasury yields reached the lowest in almost two weeks as Fannie Mae’s 3.5 percent securities climbed to 100.7 cents on the dollar, the highest since Aug. 12, before trading at 100 cents as of 10:50 a.m. today in New York.

‘Continued Overhang’

JPMorgan analysts led by Matt Jozoff said in an Aug. 23 report that they expect tapering to start next month with a $10 billion reduction in Treasury purchase and $5 billion decline for mortgage bonds, matching the median expectation of primary dealers surveyed by the New York Fed in mid-July. The poll’s results were

released Aug. 22.

“Even if taper is delayed, the continued overhang of a start sometime soon should limit” relative gains in home-loan securities, Credit Suisse Group AG analysts led by

Mahesh Swaminathan wrote in an Aug. 26 report. They recommended investors add to bets that certain bonds will underperform rate swaps and said they “assign a high probability to a September start date for taper despite the recent string of weak economic data.”